While North American carriers are driving the improved financial fortunes of the airline industry, IATA sees improvements in all other regions this year even if their profit margins remain relatively weak.

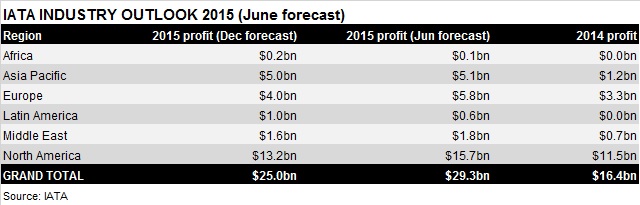

IATA projected a $29.3 billion industry net profit for 2015 in its June forecast, released during its recent AGM. This is almost double the restated $16.4 billion airlines generated in 2014.

North American carriers will again account for much of this - $15.7 billion - with European and Asian airlines generating $5.8 billion and $5.1 billion respectively.

"What we have seen is airline profits pulled up by the US. We expect over half the industry profits to be generated from the US. All other regions are seeing improvement this year. But outside the US, most regions are earning 3% profit margins," explains IATA chief economist Brian Pearce.

Lower fuel costs have contributed to the wider industry improvement, though the strong US dollar has mitigated the impact for many non US-based carriers. It has also had an impact on traffic flows.

"The strong dollar means the purchasing power of the US traveller is much higher, and we see that lead to increased outflow from the US - the US economy is still strong – and we see that as positive for passenger outflows into South America," says Pearce.

"For Europe [airline] its the opposite, but I think we are encouraged we are seeing some signs of improved confidence in Europe," he says, although he warns the region is not necessarily over the troubles is has had in recent years.

One of the most mixed regional pictures is in Latin America. While the $600 million profit Latin American carriers are set to make this year is an improvement on the breakeven performance of 2014, it is almost half the level IATA was projecting six months ago in part because of the economic challenges in Argentina and Brazil.

"Latin America is a fascinating region of many contrasts," says Pearce. "You have some airlines that perform fantastically with some of the highest margins. There are some growth spots hotspots, economies like Colombia and Chile are doing really well, but Brazil is such an important economy that it is effecting performance. That clearly will effect the performance of airlines that are exposed to that market."

The overall forecast of $29.3 billion for 2015 marks a $4 billion improvement on its forecast of six months ago. "We had a good start in the first quarter so we are already seeing the picture that we painted emerging in the first quarter," says Pearce.

"The industry is always vulnerable to shocks," he says of the challenges to achieving this profit. "The most important driver for the business, aside from what we have seen with the fuel prices, is the economy. So if we see a weakening of economic growth, then the picture looks very different. We had a blip in the US in the first quarter, but the signs are jobs are being created in the US, and although economies like China and in Asia have slowed, they are still adding a lot of income and we seen people increasing their travel."

Another profit would mark a sixth consecutive year in the black for the industry and if as forecast, the return on capital of 7.5% would see the industry earn more than its cost of capital for the first time on record. "Although this is a remarkable result for the air transport industry, it’s a common result for other industries," Pearce reminds. "Before now it has been sub-par, airlines have not been able to repay their investors."

Source: Cirium Dashboard