Hardly a month seemed to pass last year without some form of airline trading activity involving Icelanders. Buying, selling and investing in airlines, and other aviation businesses, has become something of an obsession for the island’s cash-rich financial community.

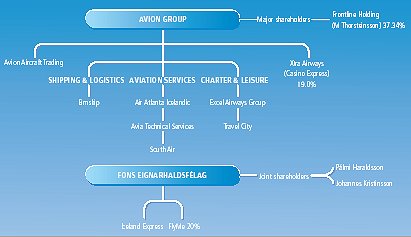

A healthy economy and stock market, one of the highest per capita incomes in the world, and financial reforms including the privatisation of the banking sector, have created Iceland’s buoyant business climate. But there are only limited opportunities at home and investors are turning to Europe. The three main players are investment companies Fons Eignarhaldsfélag, the FL Group and Avion Group.

Such predatory forays require a wealth of finance and expertise and Iceland appears to have an abundance of both. The man epitomising this spirit is Pálmi Haraldsson, co-owner and public face of investment company Fons Eignarhaldsfélag. Like most, if not all, of his fellow raiders, Haraldsson studied business practices abroad and put these to good use after returning home. Apart from the knowledge gained outside Iceland, he also singles out the wide portfolio of Icelandic investors as part of the success story. Magnús Stephensen, vice-president business development at fast-growing Avion Group highlights another ingredient in the Icelandic success story, saying that Icelanders are “somewhat more open to taking risks”.

Having acquired significant stakes in UK high street stores and speciality shops, Haraldsson turned his attention to airlines. Although he professes a particular interest in aviation, he admits that all his deals are first and foremost a business venture to make money. “I buy an airline where I can see an opportunity for cutting costs and improving the operation,” he says, “and I sell at a profit. My investing power is then further increased. There is no time limit to achieve this, but it is generally one-to-three years.”

Empire building

Haraldsson’s first foray into airlines was in August 2004 when he took an 11% stake in Swedish low-fare carrier FlyMe. It operates five Boeing 737-300s from its Gothenburg base to destinations across Europe. Shortly afterwards, in November, Haraldsson acquired a 89% stake in struggling budget airline Iceland Express for an undisclosed sum.

He then targeted Copenhagen-based budget airline Sterling Airways, which he bought from Danish shipping firms Bonheur and Ganger Rolf for just DKr400 million ($70 million) in April 2005. A further move into Denmark brought the scheduled services and charter activities of Maersk Air under his control. Haraldsson does not disclose how much he paid for Maersk Air, but since former owner the AP Møller group had found it difficult to make the relatively small airline profitable, the acquisition most likely proved a bargain.

Haraldsson immediately set about consolidating the two Danish airlines into a strong, single low-fare entity, with the aim of making it profitable by the end of 2006. The integration was completed in September 2005 with the Sterling name retained, creating the largest Nordic low-cost carrier.

Just weeks later it emerged that FL Group was already in negotiations to buy the newly created carrier from Fons. Haraldsson insists that the decision to offload Sterling so rapidly was a good business move, having achieved much in the short time in rationalising the operation. He refutes the suggestion that he baulked at the cost of revitalising the Danish airlines. There is little doubt, however, that Haraldsson made a tidy profit on the deal. Although he keeps the total cost of the Sterling and Maersk acquisition to himself, it is clear from the DKr1,500 million paid by the FL Group that it was an astute move.

Haraldsson has also been successful in turning around the fortunes of Iceland Express, so much so that the airline has attracted the attention of several Icelandic investors. According to the carrier’s chief executive Birgir Jónsson, Iceland Express now has a price tag of around $50 million and a sale is being organised. Haraldsson confirms the airline is for sale, but says that this is partly due to the fact that he acquired a 5% stake in Icelandair as part of the deal with Sterling, and having investments in both airlines has created a conflict of interest.

Iceland Express, which flies to Copenhagen and London Stansted, has announced plans to add six new routes from May 2006, serving destinations in Sweden, Germany and Spain for the first time. The airline does not have its own air operator’s certificate (AOC), but has entered into a three-year contract with Hello of Switzerland, which will provide three Boeing MD-90-30s for the expanded network. Not having an AOC, says Jónsson, “gives us the flexibility we need and allows us to be market-led. The Icelandic market is very seasonal and [this arrangement] allows us to scale our operation up or down depending on demand.” Iceland Express, he adds, is slowly backing away from the pure low-fare model and will tailor its services more closely to the requirements of the discerning Icelandic traveller.

Swedish low-cost carrier FlyMe is another typical illustration of Haraldsson’s approach to business. “The aircraft utilisation at the airline was five hours a day at a load factor of 55%,” he says. “It does not take an expert to see that there was a chance for considerable improvement. We made a new plan based on increasing production by some 150%, which in turn will cut down costs.”

FlyMe’s financial performance improved during last year, says Haraldsson, and it is embarking on a major network expansion. One of Iceland’s largest banks, Straumur-Burdaras Investment Bank, which specialises in private equity partnership investments, has a 5.2% stake in FlyMe, and has also acquired a 8.7% interest in oneworld carrier Finnair, making it the airline’s second-largest shareholder after the Finnish government.

FL’s war chest

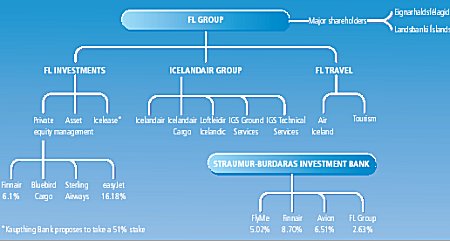

While the business acumen of men like Pálmi Haraldsson has hit the headlines, the FL Group, which has a long history in aviation, has quietly strengthened its position in the industry. Icelandair’s parent transformed itself into a major investment company in the third quarter of 2005. It then had investments worth some IKr15 billion ($245 million), with a further IKr50 billion available for further investments, with a target of a 20% return on equity. In December 2005, it raised another IKr44 billion on Iceland’s stock exchange, further strengthening its investment capability. The main focus will be on Europe, but FL says that while it traditionally has centred on travel and tourism, its horizon will now be much broader and it will not restrict itself to any specific sector.

The group’s 2005 raids included boosting its holding in UK low-fare airline easyJet to 16.18%, a stake with a market value then of around $345 million (see news story page 16); taking full control of local cargo specialist Bluebird Cargo and freight forwarder Flugflutningar; acquiring Sterling Airways, Scandinavia’s largest low-cost carrier; and buying into Finnish flag carrier Finnair, in which it now has a 6.1% stake. The Finnair shares are held by Kaupthing Bank and were acquired on a forward contract, which matures in July, but the FL Group has full voting rights since the conclusion of the contract in early January. The easyJet holding has already been highly profitable. Since buying its first 8.4% stake in October 2004 at £1.20 ($2.13) a share, the airline’s share price surpassed £4 on 9 January this year.

The Sterling deal, which was to come into effect at the beginning of this year, does have a potential stumbling block. The FL Group is “not obliged to proceed with the acquisition of Sterling, if certain conditions are not met, including, but not limited to, obtaining the necessary clearance from competition authorities.” While the Danish authorities have decided not to investigate further, Iceland’s competition authorities are still studying the move.

However, actions to turn the Sterling operation around have already begun. Its cost structure is shifting to an entirely low-fare business model through outsourcing, a greater focus on internet sales, cuts in administration costs, reorganisation of routes out of Copenhagen, currently accounting for nearly half of its network, and more efficient aircraft utilisation.

Sterling is expected to reach revenues of $820 million this year, generated from 5.2 million passengers. The business model projects a doubling of size in the next three years “that probably means another 20 aircraft”, says vice-president commercial Stefan Vilner. For 2006, Sterling will operate 30 737s.

The FL Group is also focusing on the expansion of cargo flights and aircraft trading. It has linked up with Kaupthing Bank on aircraft leasing, signing a letter of intent (LoI) under which Kaupthing proposes to take a 51% stake in the group’s Icelease arm.

This new venture will involve ownership and leasing of 15 737-800s, due for delivery in 2006 and 2007. Agreements have already been reached on five aircraft to Air China and four to Hainan Airlines, both on eight-year leases. A Boeing 747 freighter will also be leased to Singapore Airlines Cargo.

FL expects a profit of between IKr3.5 billion and IKr4.5 billion from the 737 leases. Other trading activities during 2005 included the lease of three 737-500s in co-operation with other investors, the purchase of three 757-200s and sale of four 757-200s, three of which were leased back to Icelandair, and an order for two Boeing 787-8s for delivery in 2010, with purchase options for five additional aircraft.

The acquisition of Bluebird and Flugflutningar, incorporated into FL last August after clearance by the Icelandic competition authorities, has enabled the group to place greater emphasis on international cargo flights, with the Asian market a main target. FL has set a goal of 30% growth in 2006 for its cargo operations. Two new Boeing 747-400ERFs will be acquired on 10-year leases in June 2007 and March 2008. The combined cargo fleet now comprises five 737-300Fs, two of which are owned, and two 757-200Fs.

In the first nine months of 2005, the FL Group achieved the best result in its history, recording group pre-tax profits of IKr8 billion, in spite of high fuel prices and an unfavourable exchange rate. However, Hannes Smárason, FL Group chief executive, points out that the high profit was largely due to investment income, although “the return from the operating companies was also good and in line with expectations”.

Flag carrier Icelandair is not missing out on the country’s growth surge. Traffic at the 757 and 767 operator climbed by 14.5% in the first nine months of last year. Charter and wet-lease division Loftleidir Icelandic benefited from new contracts in Cuba and Venezuela, while local airline Air Iceland (Flugfélag Islands) signed a new contract with Greenland for increased operations in this neighbouring territory until at least 2010.

Avion moves in

Another fast-growing investment company is the Avion Group, established in January 2005 through the merger of wet-lease specialist Air Atlanta Icelandic, domestic airline Islandsflug and handling company SouthAir. UK-based Excel Airways Group, now including Air Atlanta Europe, is also part of Avion, as is maintenance provider Avia Technical Services. In June 2005, it completed the purchase of shipping and logistics concern Eimskip from Burdaras, making it the largest transportation concern in Iceland.

Two months later, Avion announced the acquisition of a 19% stake in US charter airline Casino Express, since renamed XtraAirways, which, according to the group, will bring benefits “through the utilisation of Avion’s aircraft for charter projects within the USA”. Avion’s executive chairman Magnús Thorsteinsson owns another 30% in XtraAirways through holding company Mercur Investments.

In December Avion issued new share capital to bolster its war chest. The market capitalisation of the Avion Group on listing was approximately IKr68.7 billion. Group revenues this year are expected to exceed $2 billion, says vice-president business development Magnús Stephensen, adding that the company “will continue to grow, both organically and through acquisition”.

Aircraft transactions during 2005 included orders for eight Boeing 777F freighters for delivery from February 2009. Avion has also signed a LoI with Israel’s IAI for the conversion of three Air Atlanta Icelandic Boeing 747-400s into freighters. The group’s Avion Aircraft Trading subsidiary has also bought three Airbus A300-600s, which will be converted into freighters by EADS company Elbe Flugzeugwerke for delivery in 2006 and 2007.

Avion has purchase rights for a further two aircraft, highlighting the increased emphasis on cargo within the group’s fleet renewal plans, which envisage a 39-strong widebody cargo fleet by 2009. The Avion aircraft portfolio comprises 20 passenger and 22 cargo aircraft, more than half of these Boeing 747s.

The ambitious plans of Avion, in addition to Fons and the FL Group, show no signs of slowing down. But their activities could just be the tip of the iceberg. ■

GUNTER ENDRES / LONDON

Source: Airline Business